Supporters of financial globalisation argue that global finance allows investors to diversify risks, it increases efficiency, and fosters technology transfer (Kose et al. 2009). The critics point to the history of financial crises that were associated with booms and busts in capital inflows (Broner et al. 2012). In our recent paper, we argue that the risks depend on the type of capital inflow, the type of lender, and also the currency denomination of the inflows (Hoggarth et al. 2016). In line with the recent Vox column by Eichengreen et al. (2017), we find that equity inflows are more stable than debt, and foreign bank creditors are more flighty than non-bank ones. As Avdjiev et al. (2016) call for in their recent post, we also looked at more granular, currency level data. We find that flows denominated in local currency are more stable than in foreign currency. We also find evidence that macroprudential policies can help to make capital inflows more stable. This adds to the debate on the cross-border implications of domestic prudential policies (see, for instance, Buch et al.’s 2016 recent post on this).

Instruments and currency

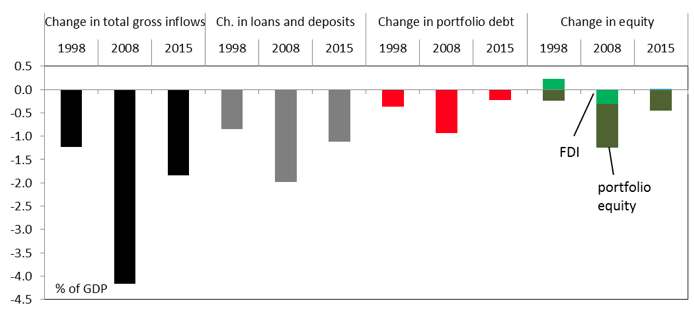

Periods of global or regional financial stress have often been associated with foreigners pulling out capital from what are perceived as risky investments, especially in emerging market economies (EMEs). Figure 1 shows the turnaround in gross capital inflows to EMEs during three episodes of financial instability: the 1997–98 East Asian crisis, the 2008–09 Global Crisis, and the more recent slowdown in 2014–15 that has not – at least so far – caused widespread distress.

This gives us a snapshot of the types of inflows that feature most prominently in reversal episodes. Loans and deposits from non-resident (‘foreign’) lenders – primarily banks – made up the largest share of the decline of total inflows in all three episodes. We also find that most of the turnaround in debt inflows to EMEs – both bank loans and marketable debt – were denominated in foreign currency.

Figure 1 The turnaround in different types of gross capital inflows to emerging market economies in periods of global financial stress (% of GDP)

Notes: Capital flows during a turnaround are the sum of the respective type of capital inflow (per cent of GDP) during a bust minus a boom. Each bust period starts in the quarter after a noticeable peak in aggregate gross capital inflows until the subsequent trough. Boom periods are the period before the bust and defined to last the same number of quarters as the subsequent bust.

Creditors

Looking at episodes when waves of aggregate capital inflows (‘surges’) turned into outflows (‘stops’) suggests that the type of creditor matters. For example, cross-border loans and deposits change a lot from periods of surges to stops, but the stops were bigger from foreign banks compared with non-bank creditors in advanced economies (comparing the dark and light blue bars in Figure 2). Also, during periods of stops in total capital inflows, portfolio debt flows into advanced economies have remained strong (the light green bars in the left-hand panel of Figure 2). This may reflect non-bank investors switching during these periods from riskier EME bonds into safe haven reserve currency sovereign bonds.

Figure 2 Debt inflows by foreign creditors in periods of country specific ‘surges’ and ‘stops’ (% of GDP)

Advanced economies

Emerging market economies

Notes: Quarterly gross capital inflows are split into two groups, conditional on whether there is a surge or stop. Each bar represents the cross-country median of the respective type of capital inflows (in percent of GDP) during periods of surges or stops in a country’s aggregate gross capital inflows. See Forbes and Warnock (2012) for details on the methodology of measuring ‘surges’ and ‘stops’.

In recent years, policymakers have been paying more attention to debt flows from non-bank financial institutions. This is partly because portfolio debt flows have become more important than bank flows since the Global Crisis, and also because non-bank financial institutions, such as asset managers, tend to be less regulated than banks. Even for EMEs, the latest data indicate that outstanding international portfolio debt, including debt issued abroad by affiliates of EME head-quartered companies, is higher than loans from foreign banks (Figure 3).

We found that about one quarter of portfolio flows to EMEs from non-banks over the past five years are from investment funds – part of the asset management industry. So we dug deeper to explore which type of investment fund inflows are the most flighty. We found that foreign currency investment funds were more prone to booms and busts than funds in domestic currency, and retail funds were somewhat more cyclical than institutional funds (Figure 4).

Figure 3 Emerging market economy outstanding cross-border bank loans and deposits and net international debt issuance

Note: The chart shows cumulative changes added (or subtracted) to (from) their respective end period (2015 Q4) stocks. Debt issuance is on a residency and nationality basis. The latter also includes bonds issued abroad by affiliates of EME head-quartered companies.

Source: BIS.

Figure 4 Emerging market economy cross-border investment fund inflows (% of GDP)

Note: Retail and institutional investor flows are defined according to the types of end-investor targeted.

Source: EPFR.

Dependence on global financial factors

We also estimated how dependent EME capital inflows are on global ‘push’ rather than domestic ‘pull’ factors. We found that debt inflows are much more sensitive than equity inflows to changes in global stock market volatility – a proxy for global risk aversion and uncertainty. As for domestic factors, inflows of loans and deposits, especially in foreign currency, were found to be positively related to domestic credit growth (pro-cyclical).

A summary of the main findings in the paper are shown in Figure 5, where the colour red highlights the least stable inflows and green the most stable ones (for more details, see Hoggarth 2016: 13). It highlights that taking the various metrics as a whole, debt flows are the least stable, especially when they come as loans and deposits from foreign banks denominated in foreign currency.

Figure 5 Summary of volatility and surges and stops in gross capital inflows to emerging market economies

We argue in our paper that policymakers are not powerless in the face of potentially volatile capital inflows. Specifically, we find that some macroprudential policies, in particular increases in banks’ capital ratios, reduce the sensitivity of loans and deposit inflows to changes in global volatility (this is highlighted in green in Table 1).

Table 1 Determinants of the sensitivity of loans and deposit flows to global volatility

http://voxeu.org/sites/default/files/image/FromMay2014/jungfig1.png

Note: The table depicts the sign and statistical significance of the interaction term of macroprudential actions and global volatility. If the sign is positive it indicates that the regulatory factor makes inflows less dependent on global volatility. The dependent variable is quarterly loans and deposit flows in per cent of GDP.

This suggests that some macroprudential policies can be used not only to increase domestic banks’ resilience against the risk of sharp changes in capital inflows, but also to reduce the volatility of capital inflows in the first place.

So, we think that the benefits of capital inflows are more likely to accrue to those countries that have in place sound macroeconomic frameworks and institutional structures. In order to help ensure that capital inflows do not cause financial instability, macroprudential measures also have an important role to play within the policy mix.

References

Avdjiev, S, R McCauley, and H S Shin (2016), “Conceptual challenges in international finance”, VoxEU.org, September.

Broner, F, T Didier, A Erce, and S L Schmukler (2012), “Gross capital flows: Dynamics and crises”, Carnegie Rochester, April.

Buch, C, m Bussière, and L Goldberg (2016), “Prudential policies crossing borders: Evidence from the International Banking Research Network”, VoxEU.org, December.

Eichengreen, B, P Gupta, and O Masetti (2017), “On the fickleness of capital flows”, VoxEU.org, February.

Forbes, K J, and F E Warnock (2012), “Capital flow waves: Surges, stops, flight, and retrenchment”, Journal of International Economics, 88: 235-251.

Hoggarth, G, C Jung, and D Reinhardt (2016), “Capital inflows — the good, the bad and the bubbly”, Bank of England Financial Stability Paper, no. 40. See also on Bank Underground.

Kose, M A, E Prasad, K Rogoff, and S-J Wei (2009), “Financial globalization: A reappraisal”, IMF Staff Papers, 56 (1).

{kind=link}